In Regulatory Notice 20-12, FINRA pointed out fraudulent emails purporting to be from FINRA officers, including Bill Wollman and Josh Drobnyk. These emails have a source domain name “@broker-finra.org” and request immediate attention to an attachment relating to your firm.

FINRA Warns Investors about Advance-Fee Scam

FINRA Disciplinary Actions Report: May 2018

Each month, the agency that regulates the financial industry, FINRA (Financial Industry Regulatory Authority), produces a detailed report that runs down all disciplinary actions recently taken against brokerage firms and brokers. We strongly encourage any investor who suspects their broker and/or broker-dealer of having lost them money on dubious terms to at least skim this report to see if you recognize any names, schemes, products, or securities.

FINRA Disciplinary Action Report April 2018

FINRA Broker Disciplinary Action Report: April & May 2016

Beware Phony Senior-Specific Investment Professionals

The law prohibits the use of senior-specialization designations by any person who lacks certification from an accrediting organization. This law makes clear that using a phony senior-specific designation that falsely implies some financial expertise in the investment needs of our elderly investors is against the law.

Securities Fraud Is A "Whole 'Nother Ballgame" For Pro Athletes

Professional athletes are among the most common targets of unscrupulous brokers and money managers. Many of these athletes, while wealthy, are also often young and inexperienced when it comes to finance and investment. Just because pro football, basketball, and hockey players have achieved an elite status in their profession does not make them any more sophisticated when it comes to investment products and strategies than the average American. However, since they do have such a high profile, they tend to attract fraudsters in much higher numbers than the rest of us. Our firm’s experience with professional athletes makes us uniquely sensitive to this situation and the struggle they face trying to recover losses when they’ve been swindled.

Accordingly, we were saddened but unfortunately not very surprised when, once again, we came across this article in the media describing how a dozen pro football players based in Florida were allegedly majorly defrauded. According to the Sun Sentinel, a group of at least twelve former or current NFL players filed claims through FINRA’s arbitration process against two Broward County financial advisors. Allegations made by the players and their attorneys include “unsuitable recommendations to invest in "illiquid, high-risk securities” in a now bankrupt Alabama casino and promissory notes offered by the parent company of Success Trade Securities.

In another case, also based in Florida and involving NFL players but this time filed in federal court, another group of players filed a lawsuit back in October alleging that a bank allowed about $53 million to be taken from players’ accounts for “illegitimate” purposes by the firm of a recently banned advisor named Jeffrey Rubin.

And that’s just recently, just in Florida. Cases like this sprout up all over the country, all the time. Pro athletes who may be unbeatable on the gridiron or on the ice need to be as careful as any other novice investor when it comes to the complex game of securities. As the saying goes, out there it’s “whole ‘nother ballgame.”

If you or anyone you know has been the victim of broker misconduct or securities fraud, please contact us immediately at 1-855-462-3330 or via email by clicking here.

Don't Become a Statistic: Fight Financial Fraud

It could be due to the fact that all day long pretty much all we do is speak to ordinary folks about how they lost their hard-earned money due to investment fraud and broker misconduct; write letters and FINRA claims about all kinds of financial scams and negligence; and educate ourselves on the latest trends in everything fishy and devious going on in the world of financial securities. BUT. This week, a couple phone calls we received and a couple articles we read brought home to us with powerful force once again just how many Americans get duped and how easy it would be not to.

photo credit Don Haskins, Creative Commons license

See, one poor lady called us up to tell us she and her husband had lost $500,000 of their retirement money because of their broker. There was only problem. Their broker wasn’t a broker. He was an insurance consultant! The phony broker is now up on felony charges. But that doesn’t help the poor couple that called us… The fake broker was broke. And since he didn’t actually work for a sponsoring brokerage firm, well, there was no one to recover damages from.

Another case involved a gentleman who had lost a lot of money because his broker had put him in a bunch of assets that were patently unsuitable for the customer. As we talked, we discovered that the gentleman, in spite of the fact that the broker had lost a sizable chunk of his portfolio, had stayed with this broker and still, believe it or not, had his money invested with him! When we asked why, he said he’d listened to dozens of brokers pitch him on why they were the right broker for him, and they all sounded the same…

Finally, the FINRA Investor Education Survey report “Financial Fraud and Fraud Susceptibility in the United States” came out the other day, with some staggering findings. Some of the highlights (or lowlights, come to think of it) include the fact that:

Over 80% of respondents to the survey had been solicited in potential scams

Over 40% of respondents could not identify classic “red flag” signs of fraud

Around 60% of respondents under-reported fraud

Around 18% of respondents had been asked to purchase an investment that offered a commission for referring other investors.

Clearly, Americans are not nearly prepared enough to recognize and combat financial fraud schemes. As securities attorneys, we are often frustrated by the fact that we can’t help people until after they’ve been bilked out of their life-savings or taken for a ride by a phony broker. And so we wanted to take a moment to remind everyone out there who is or may become an investor that the old saying, “If it sounds too good to be true, it probably is,” is about the surest way to protect yourself against investment scams. We can all be tempted. Who doesn’t want to double their money overnight? Unfortunately, far more people lose all their money thinking that way than ever double it. Do your due diligence. Just because a nice man in a suit says he’s a broker, doesn’t mean he’s a broker. Do a background check on all brokers who solicit or trade for you with FINRA’s comprehensive BrokerCheck. For more tips, tools, and techniques in our collective fight against broker misconduct and fraud, please download our free Self-Defense Guide.

As always, if you or someone you know has the victim of broker misconduct or financial fraud, please contact us immediately for a free consultation.

Naming Names: FINRA's August Disciplinary Action Report

Reading FINRA’s monthly Disciplinary Action Report is a little like reading a police blotter. There’s an almost endless list of brokers under scrutiny for trying to get away with dumb, reckless, or malevolent acts. They get investigated, fined, and/or expelled by FINRA. The report for August 2013 recently came out, and again we found the usual stunning array of villains and victims. For instance…

Wikipedia Creative Commons

One broker who allegedly impersonated his own client while on the phone with his own brokerage company in order to re-route his client’s statements to him. One would assume did this to hide massive losses from his client.

Another broker duped his own grandmother, who was suffering from dementia, into purchasing shares in a fictional company the broker owned.

Still another bad broker deceived his parents by diverting almost $1.5M in funds from their investment accounts into bank accounts he controlled.

And of course the report includes far too many brokers who convinced their customers to give them personal loans. Don’t ever loan your financial advisor money!

Normally, we soak up the FINRA report and keep an eye out for new trends and schemes in broker misconduct. But this month, for the first time, we thought we’d share. Since FINRA’s reports don’t have nearly as wide a readership as they deserve, we figured we’d run down some of the cases that caught our attention and that also might have affected more customers than those mentioned in FINRA’s summaries. In other words, if you’ve been the victim of investment fraud or broker misconduct, you might want to scan our abridged list of alleged offenders below--then take a look at FINRA’s complete list by clicking here, or try their wonderful tool called BrokerCheck by clicking right here. Enough with the build-up, it’s time to name names…

Charles Crotts, a broker based in Lexington, North Carolina and formerly of American Portfolios Financial Services (APFS) and Royal Alliance Associates, has been barred from FINRA for allegedly improperly borrowing money from clients, making unsuitable investment recommendations, and getting into some shady “undisclosed outside business activities” (hm). Read more here.

Darrell Frazier of Dublin, Ohio and formerly of Park Avenue Securities LLC, got himself barred from FINRA membership for allegedly guaranteeing customers not only protecting against loss of principal but a 7 or more percent return on their investments in a variable annuity he was promoting. Although Frazier neither admitted nor denied it, the claim also alleged that he lied to customers when they did not see their “guaranteed” return, and that he made all kinds of other glaringly unsuitable recommendations.

Based out of McGregor, Texas, Roger Fuller, formerly of Chase Investment Services, got himself barred from FINRA in a claim that stated he may have forged documents and had ownership interests in securities accounts at an executing member firm.

FINRA barred broker Jon Guay of San Jose, California and formerly of Cuna Brokerage Services, QA3 Financial Corp, and Wunderlich Securities for a claim that Guay neither admitted nor denied that found Guay taking his customers’ money for a futures trading account or to invest in a specific company only to deposit the funds, guess where, into a bank account he controlled. Guay also allegedly got involved in a dodgy mutual fund scheme.

From the Big Apple, New York, New York, Juan Carlos Parets formerly of Westrock Advisors, Joseph Gunnar & Co, and John Carris Investments, settled with FINRA and was suspended for allegedly misleading customers and omitting material in a promissory note offering. According to the claim, which Parets neither admitted nor denied, he also did not understand the product he was selling to his customers, nor was the product suitable for them.

In addition to actions taken, FINRA also provides a list of complaints that are unresolved and should therefore not be taken as an indication of culpability or guilt. But…

Richard Blair of Austin, Texas and formerly of Murchison Investment Bankers, IMS Securities, and Wealth Solutions Inc. was named in a claim alleging that Blair mislead his clients and did not put their interest before his own when steering them toward a real estate investment trust, the Cole REIT. Also, Blair allegedly provided retail customers with false or misleading forms in deals involving the purchase of those pesky variable annuities.

John Carris Investments LLC along with brokers Jason Barter, George Carris, and Andrey Tkatchenko can’t be happy about a complaint filed against them by FINRA that alleges they were involved in a highly complex and manipulative “intentional prearranged trading” scheme.

Jeremy Tintle of Atlanta, Georgia and formerly of Morgan Keegan & Company and Oppenheimer & Company will have to fight the claim filed against him by FINRA that alleges he inappropriately recommended private securities that were speculative and illiquid to a retail investor, losing her around $150,000.

If you’ve lost money and you think it may be due to broker misconduct but you don’t see your broker’s name above, please check FINRA’s complete report or enter your broker’s name into BrokerCheck.

And, as always, if you or someone you know think you’ve been the victim of broker misconduct or investment fraud, please contact us immediately for a free consultation.

Shine a Bright Light on a Dark Industry

Sunlight is said to be the best disinfectant. As investor advocates, we're all for more transparency and accountability on the part of financial brokerages. That's why we were dismayed by a recent decision by the Financial Regulatory Authority or FINRA to withdraw their proposal, originally filed with the SEC early this year, to make it very easy for investors to conduct background checks and explore the disciplinary history of brokerage firms and brokers. FINRA had been moving forward quickly with a proposal to compel all registered firms and brokers to include direct links on their websites to FINRA's free research and disclosure website called "BrokerCheck." Additionally, FINRA had also hoped to force brokers to feature prominent links to BrokerCheck on any firm-related social media pages. This last aspect of the proposal received the most push-back from financial industry executives, and caused FINRA to climb down and reassess. Brokers who criticized the proposal suggested that although they did not oppose FINRA's plan in principle, they felt that implementing especially the social media aspects would be so challenging as to prevent them from participating in social media at all. Whatever the truth of that claim, FINRA has decided to regroup and refile soon.

We hope they do. Easy access to BrokerCheck means investors will be able to "check under the hood" of prospective brokers who may claim to be clean and successful but in fact have a tarnished history of multiple complaints against them. We believe that more access and more transparency means fewer incidents of financial misconduct and fraud. This is progress. One of the reasons brokers get away with multiple acts of fraud is that there's no easy way for investors to verify the brokers own claims about him or herself. Where else can you turn to figure out if your broker, who's investing your hard-earned money, is as trustworthy and reliable as he or she or even her firm says they are? BrokerCheck is an incredible resource, and we're eager to have it available as easily and widely as possible. Hopefully, in the very near future FINRA will re-launch its proposal and shine more bright light on an industry with far too many dark corners.

If you or anyone you know has been the victim of broker misconduct or investment advisor fraud, please contact us for a free consultation.

This Investment Is a Slam Dunk--Not.

Ordinary investors aren't the only ones who get fleeced by rogue brokers, financial scam artists, and Ponzi schemers. It also happens--quite a bit actually--to professional athletes. Just because a pro ball player is wealthy and successful thanks to athletic prowess does not mean they're a sophisticated investor. That goes for wealthy and successful people in general. In other words, and even if arbitrators and juries don't always see it this way, wealth does not equal sophistication when it comes to investments and financial products. Time and again, we have seen NBA, NHL, and MLB players targeted by false friends or fraudsters who take advantage of a pro athlete's bank account or good will. A recent piece we came across on Financial Advisor strums the same sad chord.

In this case, FINRA (Financial Industry Regulatory Authority) put the kibosh on the activities of Success Trade Securities nd its CEO and founder, Fuad Ahmed, for fraudulent behavior in the sale of $18 million in promissory notes to 58 investors. Many of these investors were pro athletes. It's highly likely that these athletes invested in Success Trade at the behest of their brokers, who apparently didn't think to look more closely at the suspiciously high rates of interest the notes promised, nor at the legitimacy of the underlying business and its owner. What the brokers were looking at, we're pretty darn sure, was the prospect of making a quick buck off their baller clients. According to the report, the Success Trade notes "promised to pay an annual interest rate of 12.5 percent on a monthly basis over three years and some promised interest as high as 26 percent." Red flag, right there. As we've said before and we'll say again, if it sounds too good to be true... Case in point, Ahmed continued to raise funds to meet his goal of $5 million long after he'd already collected the $5 million. Plus, he gave himself "loans" and paid off new investors with previous investors' money (a Ponzi scheme in the making). Whether you're a pro athlete or an ordinary investor, don't let a broker or huckster sell you a piece of bright blue sky and or get funny with your money...

But if they do, and you become a victim of financial adviser misconduct or any other form of investment fraud, contact us for a free consultation. We may not be able to dunk a basketball, but we know how produce results when it comes to securities litigation.

An Injustice Lurks within the Justice System

How often do you read the fine print? Or, ok, let's make the question more concrete... Have you read our site disclaimer? It sits at the very bottom of the page there, down in the footer, in a font that's a little smaller than our body text font so as not to annoy people, and it definitely qualifies as a kind of fine print. It's ok if you've never read it. It's not like we're asking you to sign away your rights based on what's in the disclaimer or anything--we're not your brokerage company or financial adviser. Because that's basically what they do. We'll come to the point: it's just as unlikely for you to read The Green Firm site disclaimer as it is for you to read the fine print in the agreement you signed with your brokerage or financial adviser that gets you to waive your right to file a claim against them in court or to participate in a class-action lawsuit. Don't know what we're talking about? Well... Chances are you already signed the agreement without even realizing what you were giving away. And that's exactly what the brokerages count on.

Fortunately, there's been a push recently by some politicians along with an influential member of the SEC to onsider adopting new rules that would prevent or restrict brokerages from forcing customers to sign away their right to sue. As things stand, if your broker loses all your money through chicanery or negligence and you want to sue him or her and their supervising brokerage firm, you will have to take your case before an arbitration panel administered by the Financial Industry Regulatory Authority, or FINRA. No trial, no jury--just you, attorneys, and an arbitration panel. Now, brokerages like to argue (as credit card companies do as well) that binding customers to arbitration reduces legal costs and help with frivolous litigation. Well, fine, that's bully for them! But from where we sit--and it seems like more and more people are starting to agree with us--this arrangement doesn't just favor the interests of the big brokerages and advisers, it's unjust and, dare we say it, borderline UnAmerican.

Yeah, ok, we should all read the fine print. But realistically, as we demonstrated above, most people don't. This puts customers in the awful position of being fleeced not once but twice: first, when the brokerage gets them to sign away their right to sue or join a class-action suit; and then again when their advisers through negligence or misconduct lose the customer's hard-earned cash.

FINRA Is Watching, But Always Be Vigilant

This week a number of articles suggested that, as we feared, Wall Street has learned nothing from the recent financial crisis. Well, maybe not nothing. Rather than steering clear of the securitized debt responsible for the collapse of the real estate market and much of the financial market as well, Wall Street investment firms are working on new and innovative ways of resurrecting securitized financial products (you remember that stuff, right? Layer upon a layer of bad debt with an icing of good debt on top...).

Hopefully, we've all learned in the meantime to be more vigilant and skeptical of the finance world's "miracle" products. Not only that, but the Financial Industry Regulatory Authority and its CEO, Richard Ketchum, are continuing to broadcast their message of "Heightened Supervision" by investment advisors and brokerage firms when it comes to complex financial products. As Ketchum plainly warns, if broker-dealer firms want their affiliated financial advisers to offer tricky investment opportunities like options trading, variable annuities, or complex products like leveraged and non-traditional ETFs, they MUST undertake greater supervision of the advisers and of the performance of the products themselves.

For investors who have already been the victim of the misuse or abuse of one of those products, it's not just a warning: it's a chance to win money back.

As we at The Green Firm have seen firsthand in recent cases, it can often be difficult to recover money from an individual broker's misconduct. Often it's simply a matter of "you can't get blood from stone." BUT, that advisor's misconduct often extends to the supervising broker-dealer. And thanks to Ketchum's strong message, it should become increasingly easy to hold broker-dealer firms responsible for failing to deliver the kind of "Heightened Supervision" that complex financial products require, according to FINRA. Not only does this supervision apply to the proper use of specific products; it also applies to the suitability of specific products to specific investors. In other words, FINRA's concept of "suitability" dictates that there must be an affinity between the investment product and the customer. If you're a risk-averse or conservative investor, your broker should not have you invested in high-risk, complex financial products.

Finally, in the article, Ketchum mentions that, "When a broker moves to a new firm and calls a customer to say, 'You should move your account with me because it will be good for you,' the customer needs to know all of the broker's motivations for moving. In some instances, recommendations to customers can be driven by direct and indirect compensation incentives to the financial advisor and the firm itself."

We at The Green Firm would just like to remind that your own interests and the interests of your broker are not always aligned. The best protection you have against broker misconduct is free: ask lots of questions. If your broker switches employers and insists you migrate with them, be sure to ask what's in it for them.

"Home of the World's Best REIT!"

We've all seen them. Ads and billboards where business claims it's the "world's best" whatever--for some reason we instantly think of pizza or burgers. Generally we take these outlandish claims with a grain or salt (or a shake of oregano). But in the world of private placement offerings, false advertising is no joke. Especially not to FINRA. As usual, the regulatory agency is out to punish private companies who sell or attempt to sell the public any type of securities under false pretenses or based on misinformation.

A recent article on Yahoo finance reminded us to talk about what an important role advertising has to play in the securities industry, and how often advertising is used to manipulate unsophisticated investors into shady deals. For example, from the article:

Now, this is a particularly large and egregious case. But deceitful deals like this are being pitched to unsuspecting investors all the time. As we've mentioned many times before, if you're not an investment professional yourself, before you consider getting involved in a private placement or REIT like the one described above--or frankly any kind of investment offering--consult a trusted financial adviser and get their opinion first. Otherwise you could become another alarming statistic. After all, in 2012 alone, FINRA reported $10.4 million in fines from cases involving alleged advertising violations. And that's not even accounting for the tens of millions of dollars in restitutions FINRA ordered.

If, unfortunately, it's too late, and you've already been the victim of misleading advertising for securities, please contact us immediately to discuss your options.

Know Your Enemy

As a recent article in US News & World Report reminded us, investors trying to win back their money after they've been the victimized by investment advisor misconduct are, well, kind of in a rigged game. That's because, whether they know it or not, when investors open an account with a brokerage firm, they most likely are required to sign a mandatory arbitration clause that causes them to waive their constitutional right to a jury trial, and binds them to FINRA's arbitration process instead. As the article's author notes, "So far, efforts to abolish this requirement—which is inherently unfair to investors—have been unavailing. The securities industry is a powerful lobby. The last thing they want is a forum where claims against its members will be judged fairly and impartially."

These mandatory arbitration clauses present a large hurdle for individuals who have been victims of broker misconduct, since arbitrators oftentimes rule in favor of the financial industry and deny the claims of victims entirely. In fact, according to the statistics of FINRA's own website, "Results of Customer Claimant Arbitration Award Cases," over the past 5 years in cases decided by arbitrators, less than 50% saw monetary compensation awarded to Claimants (see table inset.)

nother important point is that investors who need to consult an attorney for a dispute with their financial adviser must be sure to ask any prospective attorney if he or she has experience representing customers in the FINRA arbitration process. The FINRA arbitration process contains many nuances that are unique to itself and not present in a typical commercial litigation lawsuit filed with the court.

Finally, nd in light of the award statistics cited above, it would be doubly wise to retain an attorney who has actually won a FINRA arbitration on behalf of an individual in the past. An attorney with a successful FINRA track record can not only more accurately evaluate the likelihood of winning an award, but he or she will possess the experience to know what it takes to win an award at a final hearing within this complex, opaque, and suspect system that FINRA operates and the securities industry must be grateful for.

If you or anyone you know has been a victim of securities fraud or broker misconduct, please contact us for a free consultation.

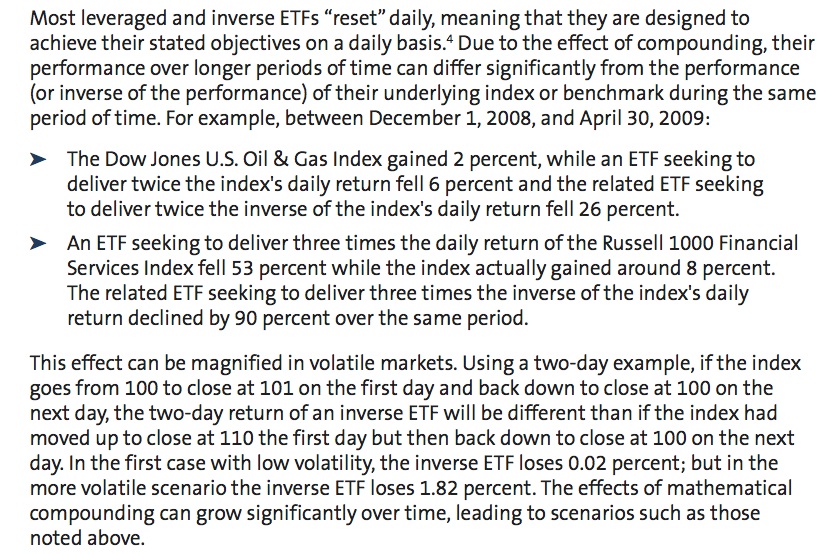

Beware of Non-traditional ETFs

SInce The Green Firm is currently pursuing a case involving a particularly egregious abuse of non-traditional ETFs, we thought it might be useful to revisit these exotic investment products and explain why they tend to be misunderstood and misused by stock brokers more accustomed to a traditional "buy-and-hold" strategy. Traditional investing principles urge brokers to "buy low and sell high." Often this means holding onto a specific financial product or stock for a long period of time while waiting for it to arrive at its "true," projected, or peak value, at which point the product is sold before it has a chance to decline. Generally, this type of traditional "value" investing is stable, low risk and low return; it also happens to be suitable for customers with a low-risk tolerance. Non-traditional ETFs, on the other, are complex, high-risk financial products that are designed to perform radically differently. According to FINRA's website, leveraged and inverse ETFs "commonly represent an interest in a portfolio of securities that track an underlying benchmark or index [not the stock market as a whole]. A leveraged ETF generally seeks to deliver multiples of the daily performance of the index or benchmark that it tracks. An inverse ETF generally seeks to deliver the opposite of the daily performance of the index or benchmark that it tracks. Inverse ETFs often are marketed as a way for investors to profit from, or at least hedge their exposure to, downward-moving markets. Some ETFs are both inverse and leveraged, meaning that they seek a return that is a multiple of the inverse performance of the underlying index." One should note that inverse ETFs are particularly tricky, since they are hedging instruments, and thus are intended to perform well in volatile markets. While a financial advisor may describe these non-traditional ETFs as a product that would be suitable in a down market, given the fact that these products "reset" daily (meaning they are designed to meet their objectives on a daily basis), even in a declining market these non-traditional ETFs should not be held for longer than one trading session. Here are some helpful examples from FINRA's Regulatory Notice 09-31:

FINRA Resolution 09-31

Many an unfortunate customer has lost money due to an uninformed or negligent broker keeping them invested in leveraged and inverse ETFs inappropriately. We have found in our cases that oftentimes the individual financial advisor does not understand the nature or use of non-traditional ETFs, and so are forced to look at the firm they work for in seeking an answer to the question of why they are investing customers in products they themselves have no grasp of. In many cases, branch managers and even the brokerage firms are not nearly familiar enough with these complex products. Clearly, ETFs can be counterintuitive and risky financial products that are not suitable for every investor, nor understood or properly used by every financial advisor or firm.

If you or someone you know has lost money as a result of improper use of non-traditional ETFs, please contact us.

SF Giants Pitcher, Barry Zito, sues for $3M

A recent lawsuit by San Francisco Giants hurler Barry Zito alleges that his friend used their relationship to mislead Zito into making a $3M investment on a fitness software startup that never materialized. We've seen misrepresentation like this before, and we're pretty sure we'll see it again. Unfortunately, pro athletes with large salaries and limited investment knowledge are highly susceptible to manipulation by stock brokers and friends alike. Precisely because they have a lot of money, they tend to be over-trusting of friends who they believe have their best interests in mind. Not always the case. And it's important to keep in mind that perpetrators of securities fraud are not always stock brokers or financial advisors--they can be anyone who enters upon a securities contract.

f you or someone you know think you've been the victim of securities fraud or misrepresentation, please The Green Firm immediately for a free consultation.